Explore Stockopedia's tools, insights and resources

Hear what our subscribers have to say about Stockopedia

Learn how Stockopedia has transformed the results of these investors

A subscription to Stockopedia will be one of the best investments you'll ever make...

Here's what you'll get:

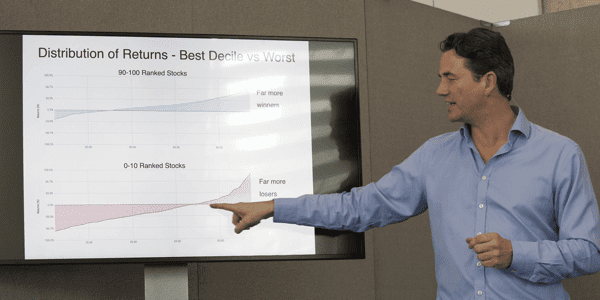

A decade of research into what works in stock markets

Millions of pounds of platform investment

Countless hours of research time saved

Access to hundreds of educational articles and ebooks

Over 30 talented professionals working flat out for you

A team of the very best bloggers acting as mentors

Saving you thousands in advisory fees every year

Stockopedia is the perfect solution for the time-poor individual investor looking for results

Starting at just £295 per year

After your free trial, plans start at just £295 per year. With a one month money back guarantee, there's no risk.